Introduction

Popularly known as the Giant of Africa and characterized by rich natural resources, diverse sectors, and a rapidly growing population, Nigeria has one of the largest economies in Africa and has gone through significant shifts over the past years. Predominantly driven by the oil and gas sector, Nigeria has faced opportunities and challenges, influencing the country’s place in the global economy. Despite her abundant natural resources, the nation’s overreliance on oil leaves the economy vulnerable as fluctuations in the international price of oil leave little to no room to absorb the shocks to the economy.

In recent times, however, efforts have been made to diversify the economy, with more focus and investments in sectors such as agriculture, technology, services, and manufacturing. The future trajectory, however, aims to incorporate renewable energy, infrastructure development, human capital investment, and sustained diversification. With a population of more than 200 million, Nigeria has opportunities and challenges – a large labour force with an immense strain on already dilapidated infrastructure and limited resources. Corruption, political instability, and infrastructure deficits, including power shortages, inadequate transportation networks, and limited access to essential services, remain some of Nigeria’s most significant hurdles to sustained economic development.

Political Influences on the Economy

A significant determinant of a nation’s economic performance is its leadership and the economic policies designed. As political parties change, a country’s economic policies often vary based on the ideology and goals of the nation’s leadership. Implementing these policies can impact areas of the economy such as monetary and fiscal policies, food security, labour crises, rising inequality, GDP, and disaster management. These economic changes can, in turn, prompt new political laws, policies, or election outcomes. According to Nairalytics, Nigeria’s economy grew the most under the 2-year presidency of late President Umaru Musa Yar’adua between 2008 and 2010 and grew the least under President Muhamadu Buhari from 2015 to 2023. The robust economy during Umaru Yar’Adua’s administration {2007-2010) in Nigeria was primarily attributed to high global oil prices, economic reforms promoting diversification, debt relief, prudent fiscal policies, investments in infrastructure, and relative political stability, while President Buhari’s administration grappled with economic challenges and high poverty levels due to factors including the impact of declining global oil prices, slow economic diversification, poor policy implementation, security concerns, and inadequate infrastructure.

Economic Policies

During the Goodluck Jonathan administration, the Transformation Agenda was launched, which aimed to diversify the economy and reduce dependency on oil revenue. The policies of the Transformation Agenda impacted various sectors of the economy. By 2013, the importation of food into Nigeria was decreased by 40%, a new minimum wage of N18,900 was implemented, nine new federal universities were established, it also birthed the 35% Affirmative Action for women in politics, giving room for more women to participate in politics. The result was an increase in non-oil exports to $ 2.9 billion by the end of 2013 and a GDP of over $570 billion, making Nigeria the largest economy in Africa under his watch.

In 2015, President Muhammadu Buhari took over from President Goodluck Jonathan; dealing with falling oil prices, corruption, and security issues, he introduced The Presidential Initiative on Continuous Audit (PICA) to tackle corruption in public offices. Other policies include the Anchor Borrowers Program (ABP), Trader Moni, the National School Feeding Programme, the N-power initiative, and the controversial Naira redesign policy. These policies needed to have been adequately implemented and better monitored, however, they resulted in increased unemployment and a reduction in the standard of living. President Tinubu, during his inauguration, announced the removal of subsidy from Premium Motor Spirit (PMS), commonly known as petrol, immediately impacting the economy and the people. As expected, petroleum product marketers promptly increased the pump price of petrol to N540 per liter, leaving Nigerians aggrieved as the cost of transportation increased drastically. The administration also touched on the monetary policy reforms, which led to the Central Bank (CBN) discarding the multiple foreign exchange FX rates it had to maintain a unified exchange rate. The positive impact of these policies has yet to be felt, though Nigerians eagerly await and hope for the anticipated economic transformation.

Global Crisis Impact

Aside from political influences, over the past 17 years, the Nigerian economic landscape has also been impacted by some global events. From the 2008 global economic crisis to the 2014 oil price slump and the unprecedented challenges of the COVID-19 pandemic, Nigeria faced formidable hurdles, including the fluctuations in global oil prices and the nation’s extreme dependence on oil resulted in increased inflation, a weakening of the local currency, and a high cost of living. The effect of this dependence on oil has now led to a rising interest in the non-oil sector as a means of diversifying the economy.

Drivers of the Economy

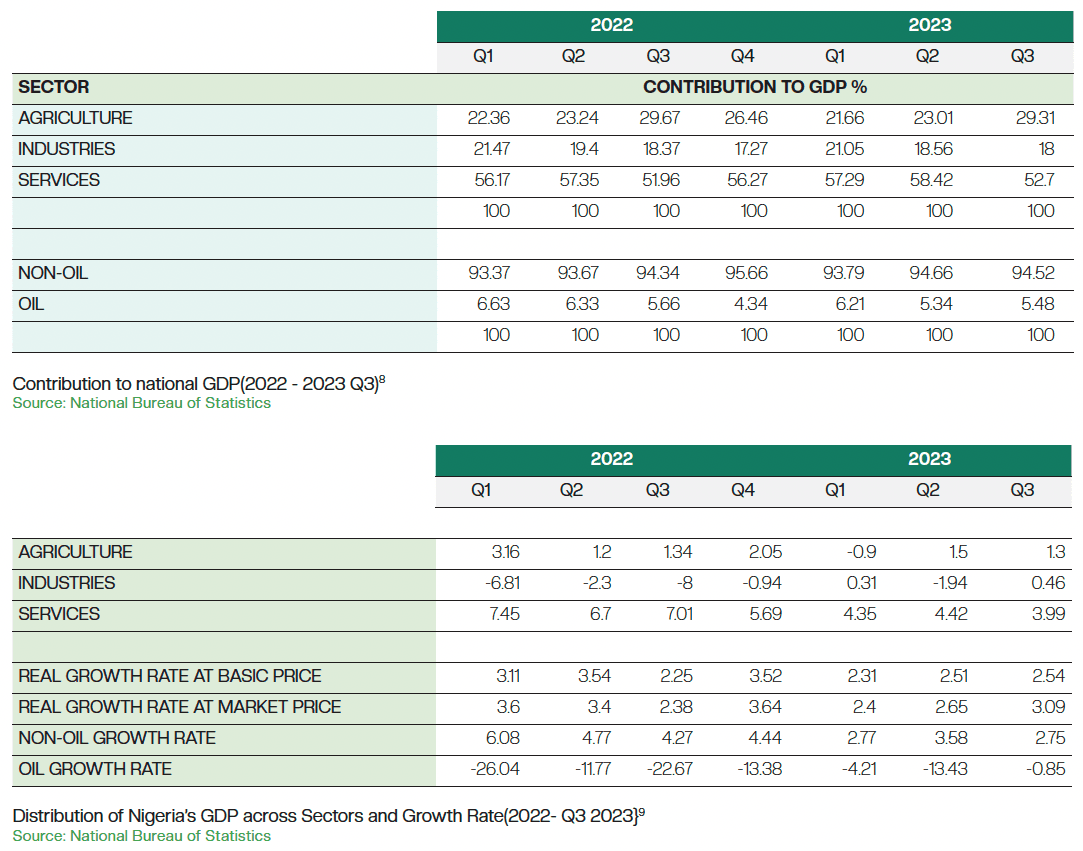

Recognizing the risks of over-dependence on oil, efforts have been made to boost other sectors like agriculture, manufacturing, and technology to create a more balanced and resilient economic base. Agriculture has always played a crucial role in the Nigerian economy. Also, the services sector, including telecommunications, banking, and entertainment, has experienced notable growth in the Nigerian economy. In a National Bureau of Statistics report, the service sector contributed 52.70% to Q3 of 2023 aggregated GDP.

Solutions and Recommendations

In a research conducted by Ciuci, Nigerians’ main challenges currently faced revolve around an increased cost of living. When asked how much he had saved in 2023, one of the interview respondents said, “I was only able to save N12,000, and I have spent it.” Another respondent said, “As you’re saving, you’re spending, so there’s nothing to keep.” Given the high cost of living, there needs to be more support for entrepreneurs in the nation. Efforts to diversify the economy have made entrepreneurship a potent solution to economic challenges, propelling individual success and national development. In the broader context of economic growth, entrepreneurs play a pivotal role in fostering innovation, creating employment opportunities, and driving overall prosperity.

Their ability to identify market gaps and introduce novel solutions meets consumer needs and stimulates healthy competition, promoting efficiency. To foster entrepreneurship, supportive measures are essential. First, education and training programs should be accessible, imparting practical skills and cultivating an entrepreneurial mindset. Access to capital through grants and venture support is crucial for turning ideas into viable businesses. Streamlining regulatory processes, promoting a risk-tolerant culture, and creating networking opportunities create a conducive environment. By embracing these recommendations, there will be fewer dependencies in the oil sector, and societies can cultivate a vibrant entrepreneurial ecosystem, ensuring sustained economic development and resilience in the face of evolving challenges.

The government should also prioritize the diversification of industries, reducing reliance on singular sectors for stability. Implementing prudent fiscal and monetary policies is essential for economic resilience. Investment in education and workforce development ensures a skilled labor force capable of adapting to evolving market demands. Collaboration between nations on a global scale facilitates knowledge exchange and broader economic opportunities. Collectively, these strategies contribute to building a resilient economic foundation.

Conclusion

Nigeria’s economic journey reflects a complex interplay of historical overreliance on oil, political influences, andglobal crises.

Political transitions and international challenges have shaped policies and outcomes. Amidst persistent hurdles, entrepreneurship emerges as a crucial solution, supported by initiatives promoting education, capital accessibility, streamlined regulations, and global collaboration.

The collective efforts to diversify industries, implement prudent economic policies, and invest in education are poised to establish a resilient, diversified financial foundation for Nigeria’s sustained growth and adaptability to evolving challenges.